If you’re here because you searched “Zelle app discontinued”, odds are something simple went sideways. You opened your phone. You looked for the Zelle app. And it wasn’t there.

So your brain did what any reasonable brain would do: Did Zelle just shut down?

Short answer: no.

Longer (and more annoying) answer: Zelle didn’t disappear — it moved, quietly, and without doing much to explain itself.

What “Zelle app discontinued” actually means (and why everyone got confused)

Here’s the part Zelle never made particularly clear.

When people say “Zelle,” they’re usually talking about one of two very different things — and mixing them up is where all the confusion starts.

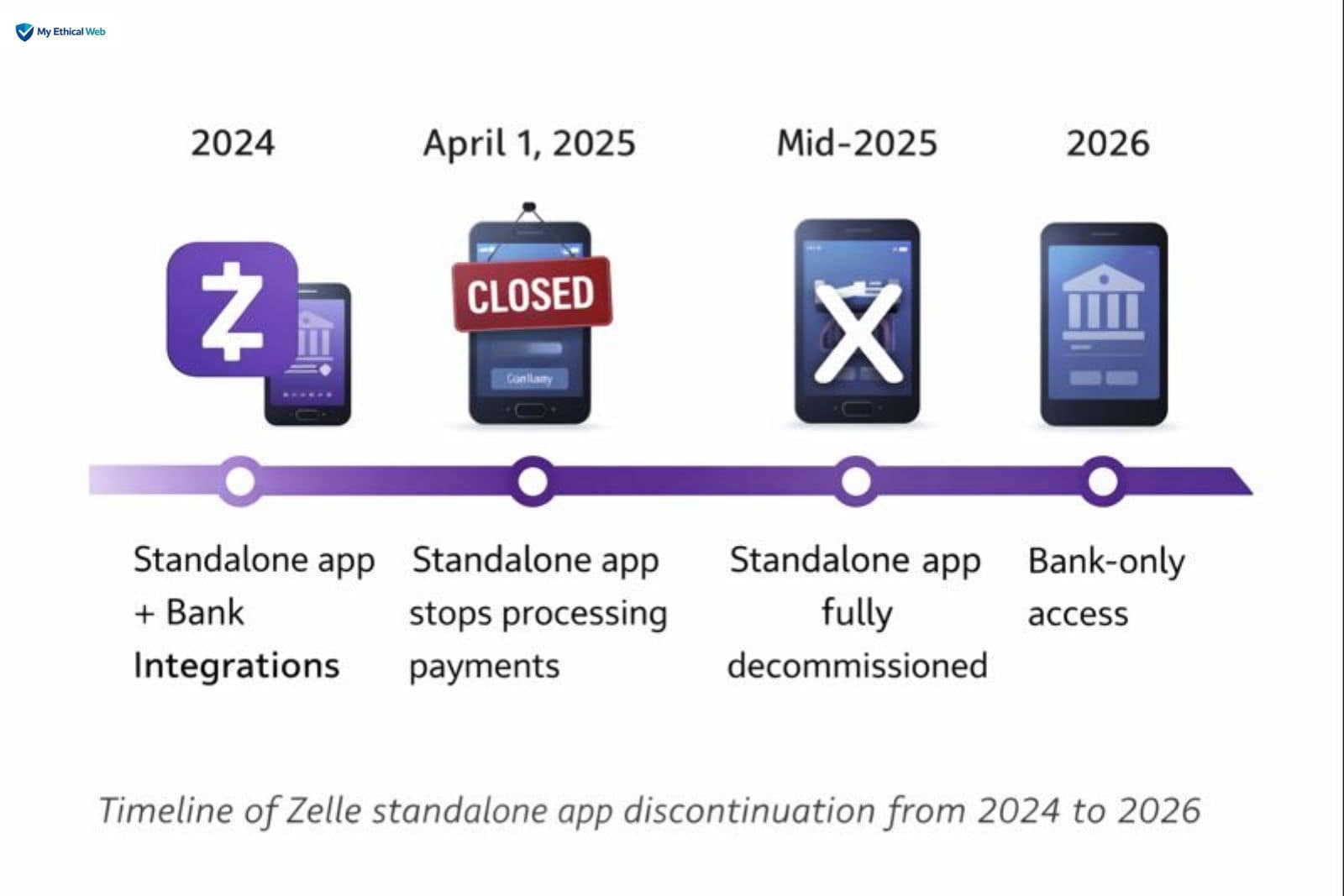

The Zelle app — the standalone consumer app you could download from the App Store — is dead. Fully. As of April 1, 2025, it stopped sending and receiving money, and by mid-2025 it was decommissioned entirely.

The Zelle network, though? That’s still very much alive in 2026. It just lives inside participating bank and credit-union apps now, instead of existing on its own.

Here’s what actually happened: Zelle pulled the app, but kept the plumbing. Payments still move. Money still lands fast. You just don’t interact with Zelle directly anymore — your bank does that for you.

And that shift? That’s what tripped everyone up.

While people were hunting for an app icon, Zelle had already turned into infrastructure — functional, invisible, and easy to assume was gone.

Why Zelle killed the app (and why “low usage” isn’t the whole story)

Zelle’s official explanation leaned on a tidy stat: by late 2024, roughly 98% of Zelle transactions were already happening inside bank apps, not the standalone one.

That’s true. But it’s not the full picture.

Around the same time, pressure was building from all sides — regulators, banks, and consumers — over authorized push payment scams. The kind where users technically approve the payment, even if they were manipulated into doing it.

That distinction matters more than most people realize. Because once a payment is “authorized,” reimbursement rules change. Liability gets fuzzy. And when something goes wrong, the question becomes uncomfortable fast: Who’s actually responsible here — Zelle, or the bank?

The standalone app sat right in the middle of that mess. Users saw Zelle. Banks absorbed the fallout.

By pulling the app and forcing all Zelle activity through bank-controlled interfaces, that ambiguity disappeared. Banks now own the warnings, the confirmations, the limits — and the consequences.

Cleaner structure. Clearer liability. Less finger-pointing.

What changed for users once the app vanished

On paper, not much. In practice? Plenty.

Zelle still moves money quickly, but the experience now depends entirely on where you bank — and banks are not consistent creatures.

After the app disappeared, your bank took over everything: daily limits, warning screens, confirmation steps, even how disputes get handled. Some banks barely touched the experience. Others buried Zelle three menus deep and added so many confirmation prompts it feels like you’re wiring money to a foreign government.

Same network. Very different vibes.

And that inconsistency is why Zelle feels “off” to people now, even though it technically still works.

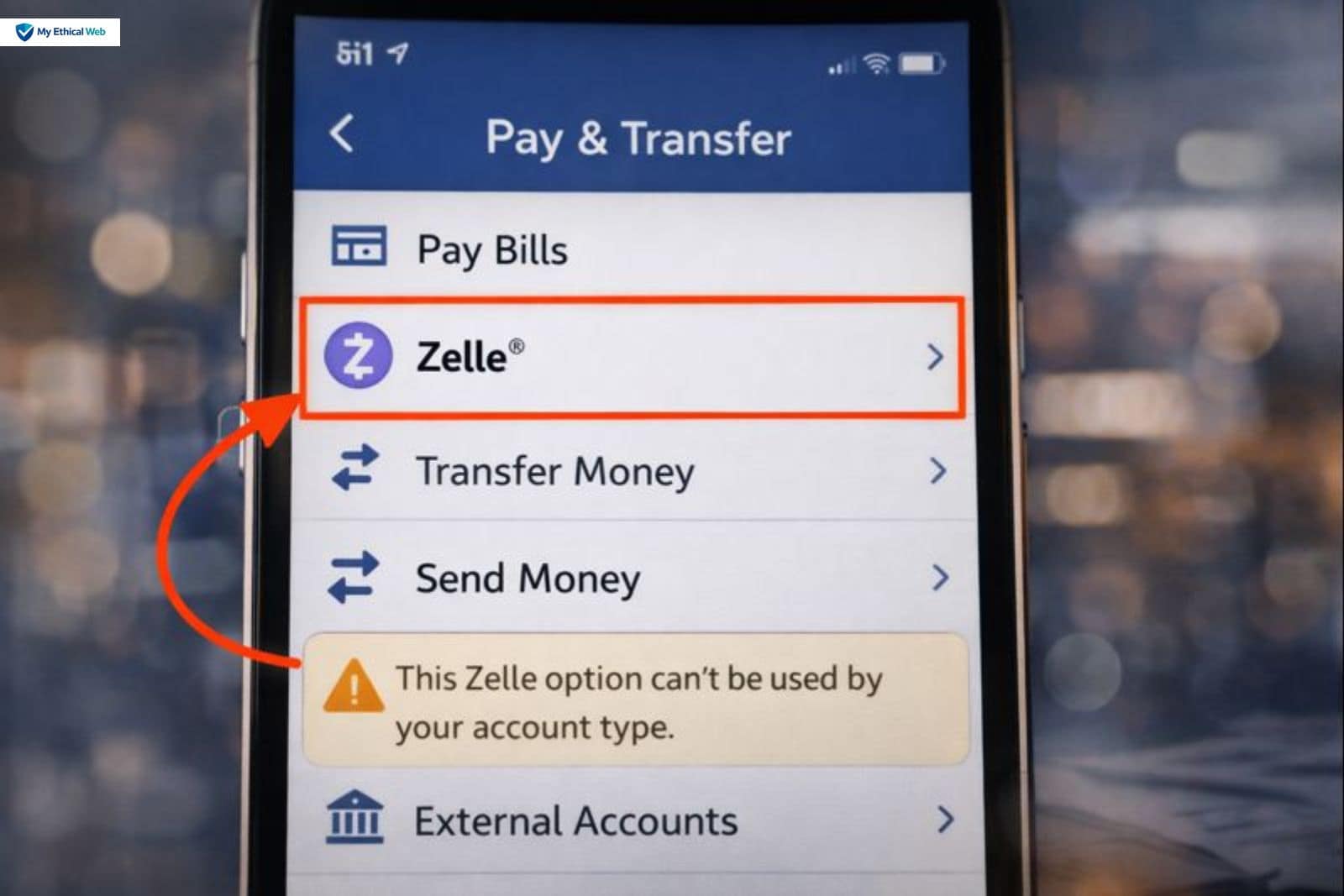

“But my bank shows Zelle — why can’t I use it?”

This is where things get weird (and honestly, a little sloppy).

In 2026, some banks will happily show a Zelle option in the app even if your specific account type can’t actually use it. Brokerage-only accounts, limited checking products, or newer fintech hybrids are common culprits.

So you’ll see “Zelle” under Payments, tap it, and hit a wall — error messages, upgrade prompts, or vague instructions to “contact support.”

It’s like a locked door with a handle that still turns. Seeing Zelle in the menu doesn’t always mean it’s usable.

If your bank doesn’t support Zelle anymore, you’re out of luck

This is where the app shutdown stopped being cosmetic.

Back when the standalone app existed, it acted as an escape hatch. Your bank didn’t support Zelle? No problem — just use the app.

That door is closed now.

If your bank or credit union doesn’t integrate Zelle in 2026, you simply cannot use the service. Full stop. You can check if your bank supports Zelle by searching for your financial institution on Zelle’s enrollment page.

Your options narrow quickly: switch banks, use Venmo or Cash App, or fall back to traditional bank transfers. If you need help choosing between payment apps, here’s a detailed comparison of payment app features that covers Zelle, Venmo, Cash App, and PayPal.

For some users, Zelle didn’t just change. It ended.

A heads-up if you’re hunting for old Zelle records

This one caught a lot of people off guard.

If you used the standalone Zelle app in the past, your transaction history did not migrate into your bank app. Zelle gave users until August 11, 2025 to download those records manually.

Missed that window? Yeah — that’s where people get genuinely angry.

You need proof of a payment from eight months ago for taxes or a dispute, and the data just… isn’t there anymore. Your remaining options are contacting Zelle support or working with your bank to recover transaction details from their records.

Not elegant. Not fun.

So why does Zelle feel different now?

Because it stopped behaving like a product.

When a branded app disappears, trust shifts — even if the service underneath keeps running. Payments rely on confidence as much as mechanics, and Zelle traded visibility for control.

It didn’t die. It just stopped introducing itself.

The bottom line (Zelle in 2026)

Here’s what actually matters: Zelle still exists, but only through participating banks. There is no standalone app anymore. Your experience depends entirely on your financial institution. And if your bank doesn’t support Zelle, you’re done.

Once you understand that shift, the confusion finally makes sense.

To protect yourself while using any payment app, the FTC provides guidance on recognizing payment scams and the CFPB explains consumer protections for digital payment services.

FAQs

Q. Did Zelle actually shut down, or did something else happen?

Zelle didn’t shut down — but the way most people used it did. The standalone Zelle app was pulled in 2025, which is why it suddenly vanished from phones. The payment system itself kept running, just quietly folded into bank apps. If that feels like a half-shutdown, you’re not wrong.

Q. Why can’t I find the Zelle app anywhere in 2026?

Because there isn’t one anymore. There’s nothing to reinstall, nothing hidden in the app store, nothing you’re missing. If your bank supports Zelle, it lives inside your banking app now — usually under payments or transfers — and if your bank doesn’t support it, that’s the end of the road.

Q. Can I still use Zelle if my bank doesn’t offer it?

No. And this is where people usually get annoyed. The standalone app used to be a workaround for banks that didn’t integrate Zelle. Once that app disappeared, so did the workaround. In 2026, no bank integration means no Zelle, period.

Q. Is Zelle safer now than it used to be?

Sometimes. Maybe. It depends entirely on your bank. Since banks now control the screens, warnings, and limits, some tightened things up while others barely changed anything. Zelle didn’t magically become safer overnight — the guardrails just moved into your bank’s hands.

Q. Why does Zelle feel harder to use than before?

Because it stopped being one thing. What used to be a single app is now dozens of slightly different versions, depending on where you bank. Some banks made Zelle easy to find. Others buried it. Same network, wildly different experiences — and that inconsistency is what people notice.

For more insights on navigating digital services and understanding how technology shapes everyday life, visit My Ethical Web.

| Disclaimer: This article is for informational purposes only and does not constitute financial, legal, or professional advice. Payment app features, bank policies, and service availability may vary and change over time. Readers should verify current information with their financial institutions and consult qualified professionals for specific guidance regarding their financial transactions and account management. |